Update 3/30/2019: I no longer use StashWealth and instead of switched to Vanguard. Everything about this review still stands — it was a reflection of how I felt at the time. For a brief explanation on why I switched, read this. I will write a more detailed article on the decision in the future.

When I was 14, I started packing take-out orders at a Chinese restaurant.

I’d stand in the oppressive kitchen in poorly fitted dress shirt from TJ Maxx for 7 hours and box ubiquitous white boxes of Chinese food. I’d put an X on the check, then sort and drop different sized boxes into a brown paper bag, like Tetris.

When I got home, I’d take my pay — $20 — and stuff it into a brown wallet, tucked in my sock drawer.

I asked my parents what I should do with my money.

“Save it,” they said.

Months later, I started waiting tables at the same restaurant. The $20 turned to $100 per night. I worked weekends during school, weekdays in the summer. When the wallet was bulging with $20 bills, I traded them for $100 bills.. When it bulged again, I held the wallet together with a rubber band.

I asked my parents what I should do with the money.

“Invest it,” they said.

I did. Some investments paid off, others didn’t (stupid CROX). I stopped waiting tables and took other jobs. For a long time, I made less money. Eventually I made more. Regardless of how much I made, I saved and invested.

When I turned 30, I asked my dad, what should I do with my money?

“Honestly, I don’t have much more advice for you,” he said. “You know as much about handling your money now as I do.”

That’s when looked into StashWealth.

What is StashWealth?

StashWealth is a financial planning service that focuses on money advice for millennials. Founded by Priya Malani and Rob Kovalesky, StashWealth bills itself as “not your father’s financial advisor”, and use the acronym HENRY to describe their customers (High Earning, Not Rich Yet). The messaging doesn’t resonate with me (more on that later) but at least they have a clear audience.

Here’s how their financial planning services work:

The first step is coming up with your “Stash Plan.” They help you think about your goals, then work backwards from your goals to your current financial situation, to create a plan of attack.

From their website, here’s what’s included in the Stash Plan:

- Evaluate your current situation

- Optimize credit cards, student loans, 401(k), stock options, emergency fund, etc

- Uncover your financial goals

- Help you automate your savings

- Consolidate your financial accounts

- Develop an investment strategy to make your money work harder for you

- Answer all your money-related questions, including how to save on taxes

You get 3 calls with your financial advisors to build out this Stash Plan. On the last call, they walk you through your customized plan. Then, you can implement the plan yourself, OR you can sign up for Stash Management, where they’ll execute the plan for you:

“We manage the execution of your Stash Plan™ and are available to answer any questions that come up throughout the year. We will check in on you from time to time and give you a heads-up if there’s anything you need to be thinking about. Each year, we’ll touch base on the big picture and recalibrate your Stash Plan™ as needed.”

So with the incredible amount of free information on wealth management out there, and plenty of low-cost robo advisor options, how did I end up using StashWealth?

Money is a game, learn to master it

In highschool, my macroeconomics teacher taught a one-day lesson on personal finance for millennials. It was the best class in 4 years. 13 years later, I still have the notes from that day:

It was the first time I realized that money — making it, spending it, and managing it — was a game. There were rules, strategies, and levels.

I decided to become a student of the game. So I started reading.

Personal Finance for Dummies (which was better than expected). The 9 Steps to Financial Freedom by Suze Orman (which wasn’t). Rich Dad, Poor Dad. One Up on Wall Street. A Random Walk Down Wall Street. This financial automation video, from Ramit Sethi:

One tax season, I wound up owing $10,000 in taxes. I decided to create a tax “playbook” so that wouldn’t happen again. I kept building my foundation. But in my mid-20s, I realized something was missing.

You see, most games break down to 3 stages: Opening, mid-game, and end-game. Chess follows this structure. So does poker, backgammon, and Brazilian jiu-jitsu.

Business is a game. Marketing is a game. And so is money.

There are openings, mid-game moves and end-game moves — a beginning, middle, end. And while I felt strong about my openers (savings, budgeting, automation) and end-game (saving for retirement) there was a big hole: the mid-game.

Arguably, the mid-game is the most complicated part. No one will argue that saving money is bad or that you shouldn’t invest for retirement. But everyone’s got a different opinion on the mid-game. That’s because everyone approaches it from a unique place, with different amounts of money saved, debt accrued, and financial baggage. For example, a ton of my business school friends went straight into accounting and banking and made a ton of money their first 5 years after graduating.

I dropped out of business school, waited tables, and worked for free instead.

This is where we have to make some of the biggest decisions of our lives… yet there’s no one to help us with questions like:

- If I want to buy a house in 3 years, how much money do I need?

- Should I keep the money as cash or invest it?

- Am I even buying a house for the right reasons?

- If I’m ready to start a family, when do I think about saving for that?

- I have money sitting in an old 401(k), what should I do with that?

- What does asset allocation for a 30 year old look like?

- What do people in their 40s wish they knew in their 30s?

- What else should I be saving for?

- What are the real, best millennial money habits to establish now? What don’t I know that I don’t know?

These were questions I looked towards StashWealth to answer.

Unfortunately, I nearly quit their service before they got the chance.

My honest StashWealth review

This StashWealth review gets off to a rough start.

Couple reasons for that:

When working with the StashWealth financial advisors, your first step is setting up your automated system. Your homework is creating sub-savings accounts (like an emergency fund) and making sure funds divert there automatically. If you’re new to personal finance, this is essential.

But I wasn’t new, and I’m always trying to level-up (check out my review of my most recent course, Ramit’s How to Win the Game of Advanced Personal Finance). And (I thought) my financial advisors knew that. Yet still we went through the exercise. The first 2 calls were a rehash of everything I learned years ago.

Frankly, it felt like a waste of time.

Here’s the second reason why I this StashWealth review gets off to a rough start:

Personally, the “brand” behind StashWealth never resonated with me: Being referred to as a HENRY. Being told I was on my way to becoming a millionaire. Things like that.

During the planning stage, they told me to think aspirationally. If I wanted to save and eventually splurge for a Tesla, a yacht, or a SoHo House membership, then write it down and plan for it. “Think BIG!” they said.

I understand WHY they do it. I understand they’re building a brand. And it’s important to paint a picture of success for your customers. Perhaps the “average” millennial, when they aren’t ruining chain restaurants or eating avocado toast, IS dreaming about a Tesla or their country club membership.

But for a service billed as a personal experience and plan, it felt very impersonal. Because personally, I don’t give a shit about cars. My “dream car” used to be a station wagon (now it’s a minivan). I don’t care about boats. And unless we’re catering the food, Chinese people don’t do country clubs.

Those first 2 calls were so off-putting, I remember debating whether or not to cancel the third call.

I’m glad I didn’t.

What I love about StashWealth

StashWealth completely recovered by the third call — and ever since.

Maybe that’s just how it goes. Or maybe they sensed the aspirational bit wasn’t landing. Either way, on the third talk, the tone shifted. We got into the meat.

The personalized plan was terrific. Rob Kovalesky and Mary Nosuchinsky went through my goals, one-by-one, and showed me where I needed to move every dollar if I wanted to hit those goals. When I raised objections, they empathized, but gently explained why my thinking was antiquated, or plain wrong. In one call, I felt like they completely reworked my financial game.

I finally had a sense for my mid-game strategy. Plus, a plan to execute it.

Here are the highlights from the call:

(1) Personalized, actionable advice. It took 3 sessions, but it was worth it: The plan they came up with was 100% customized to my needs. They made several recommendations: Start using my wife’s Roth 401(k) for the tax deduction, use 529 college savings plans if we chose to stay in NY, etc. But one of the most eye-opening recommendations was simple:

Stop keeping so much of our money in cash.

The Reformed Broker has this post called “Opposite Day.” Basically, the idea is one of the worst millennial money habits is keeping too much of their assets in cash, and not putting enough into the market. Which is exactly what I was doing.

Rob Kovalesky asked why so much money was in cash.

“We’re thinking about some big purchases soon. We started a baby fund. We want to buy a house. Plus, I’m always worried about having enough cash on hand to cover the credit card payments in full.”

Rob said that made sense. “But that’s why you have an emergency fund.” He explained that an emergency fund isn’t all the cash you’ll ever have on hand. Instead, think of it as the first line of defense. “If you need more cash, no problem, we’ll move things around for you and get more cash.”

That was a total mindset shift. In 10 years, I never considered that.

(2) StashWealth told me exactly how to reallocate my money. Like I said, our automation system was set up… the problem was the money wasn’t properly allocated. I’d known this for years and never did anything about it. They made strong recommendations on getting the money to the right places, which meant closing some accounts and consolidating others. If we needed to open accounts, they handled the paperwork and opening procedures, and just told us how to reroute funds.

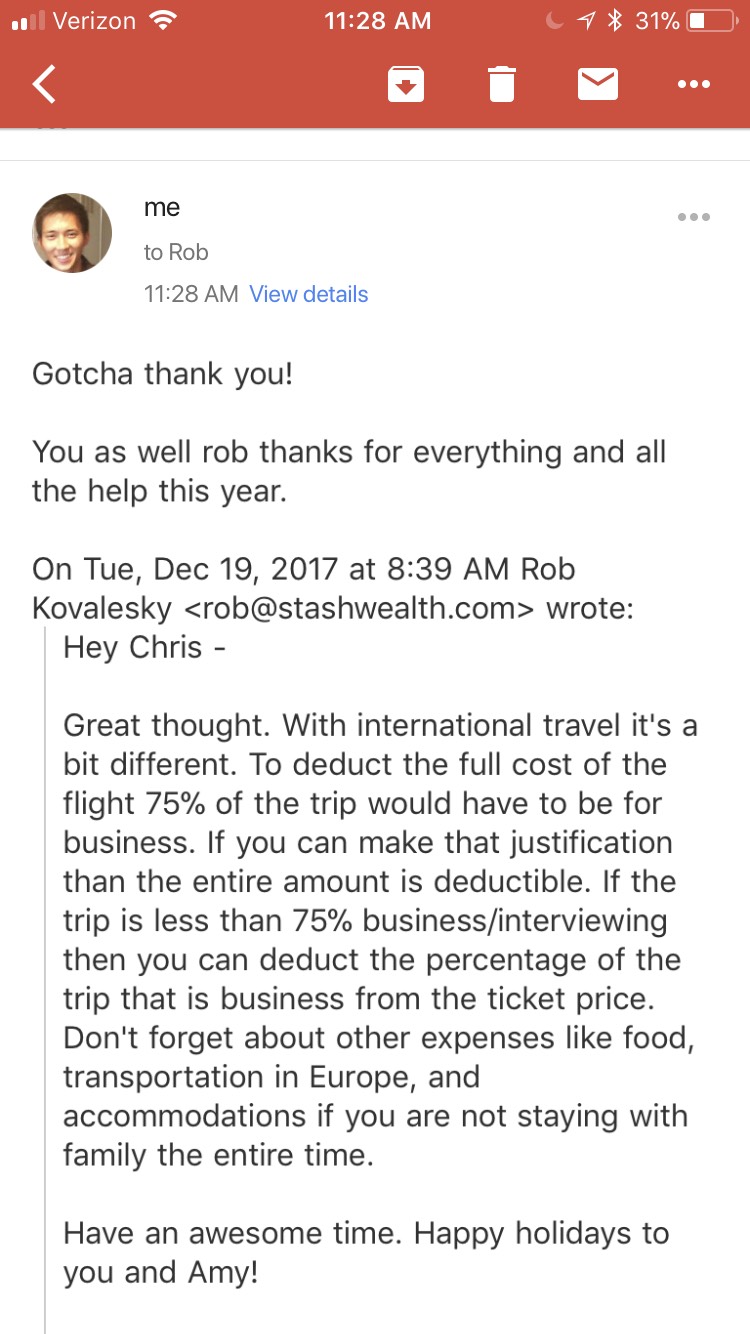

(3) Crazy good response rate. Since that call, anytime I’ve had a question, Rob or Mary answered it in a few hours. Not a customer support person, and not via messenger bot: Just plain old email, typed by a human being.

Here’s an example of a response Rob sent 20 minutes after I emailed him first thing in the morning:

Robo advisors vs financial advisors

I think robo advisors (like Wealthfront, Betterment, or WealthSimple) are great tools. They have low fees and from what I hear, both Wealthfront and Betterment get solid returns.

But in my opinion, they don’t address the mid-game issues. I used Wealthfront in the past, and each time I’m on the dashboard, and it shows me how much my investments will be worth is 40 years. Which is great…

However, what about in the meantime? Forget retirement, forget what compound interest does in 40 years… what about the next 4 years? The best robo advisor can’t give you personalized advice.

I’m sure Wealthfront has the tools for me to learn the mid-game on my own. I could have figured it out. Except the fact is, in the last 10 years, I hadn’t done any research, or changed my strategy, or even tried to solve the mid-game. Past behavior is the best indicator for future behavior, and it’s more than likely I’d continue to do nothing for the next 10 years.

There was a time when I’d take 5 minutes to write down every transaction, by hand, on a sheet of paper.

Went to work at the restaurant? Put $20 in the credit column.

Buy something? Take it out in the debit column.

Every 6 months, I’d schedule a 15 minute call with my credit card company to ask for an credit increase, to improve my credit score. I’d spend a whole week reading the newest money book.

That work laid the foundation, but today, it’s not where I want to invest my time. It’s certainly not enough to keep up with today’s mid-game challenges. By the time you figure out how to pay your rent on time, you’re thinking about buying a house. When you’re settled into your job, you decide to start a side business. Or when you’re finally making a comfortable living for two, you get pregnant.

In the mid-game, the changes come fast, and you’re getting pulled in all directions. I don’t think the best robo advisor can help you solve for those problems. So if you can get help — personal, real-person help where you can bounce ideas off and whose default answer isn’t “index funds” and “tax harvesting”… why wouldn’t you?

Is StashWealth right for me?

It’s not for everyone.

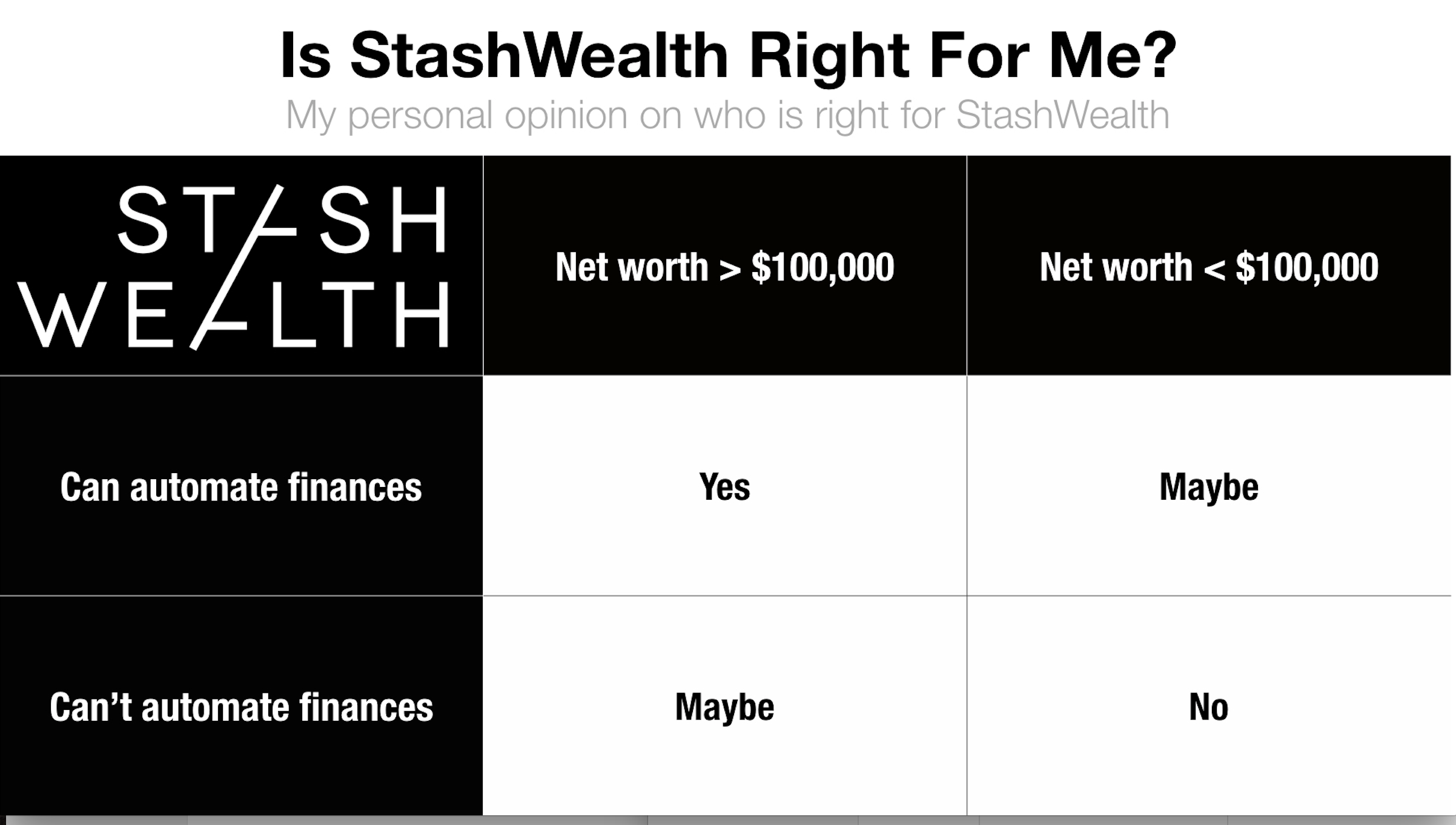

Here’s my personal opinion on who is right for StashWealth:

Here’s why I break it down this way:

Can execute financial automation. In other words, you understand how your paycheck should flow — automatically. A simple example: $ from gross paycheck goes directly to your 401(k). The rest hits your checking account, then flows to your savings and fixed expenses. The rest you can spend.

If you can’t set this up yourself, solve this first.

StashWealth can help you do this. However, there’s something visceral about connecting the dots on your own, and studying the flow of your own money. Even if it takes 6 months to get it right, it’s time well spent. The better you understand the machinations, the more you appreciate your money.

When I tracked my money in a college-ruled loose leaf ledger, I respected every dollar that hit my wallet. Especially because I was paid in cash: dirty, stained bills flung onto tables or carefully tucked under porcelain teacups. I grabbed them with sweaty palms and stuffed them into my apron. When I bought something and forked over the cash, I didn’t measure it in dollars, but days, spent stuck in the restaurant. The Dunkin Donuts fruit coolatta cost me 20 minutes. Adidas Superstars, half a day. A brand new pair of glasses cost a whopping 3 days.

Once you establish a baseline understanding of the machinations of your money, and then you want help, great. In that case, I couldn’t recommend StashWealth enough. They’ll help you execute the finer details of your financial plan.

For example, logically I know asset allocation is 80% of the investing battle, but I constantly put off figuring it out for “later.” There’s plenty of advice out there on asset allocation for 30 year olds, but “later” turned to “years”… and still I did nothing.

Once I handed it off to StashWealth, they made their recommendations on asset allocation, I agreed, then we were on our way. And because I had that baseline understanding of my own finances, I could evaluate their recommendations with confidence.

$100,000 Net Worth. StashWealth isn’t competing on price. Here’s how the StashWealth fee stacks against robo advisors fees:

- Wealthfront fee: 0.25%

- Betterment Premium fee: 0.40%

- WealthSimple fee: 0.40%

- StashWealth fee: 1.2%

If you’re price sensitive, you’re looking for bang for your buck, then you can’t beat the robo advisor fee. And in my opinion, if your net worth is less than $100,000, you should be price sensitive. Buy I Will Teach You to Be Rich by Ramit Sethi (note: I used to work for Ramit), pay off your debts and automate your funds. Invest in your 401(k), your Roth IRA, and with money left over, a Vanguard Index Fund. For many, this is a terrific 80% solution to aim for.

Life gets complicated. StashWealth makes it less so

As your financial literacy and net worth increase, you reach this point where cost sensitivity decreases, but time sensitivity increases.

In other words, life gets complicated. StashWealth makes it less so.

Choosing StashWealth wasn’t about making more money and saving more time, today. It’s about earning money and saving time 10, 20, even 30 years from now. Because from here, life only gets MORE complicated.

I’ve been lucky to work with many successful people, in different industries: Restaurant, entertainment, publishing, tech. What I’ve learned is, no one ever “figures it all out.” There’s always another challenge, whether it’s financial, career, or personal: mortgage payments, property tax, child care, people die, jobs get lost, or fucking cancer. Yet as things get more complicated, we have less and less time to research the options and weigh the pros and cons. Which is precisely why you’ll prefer financial advisors vs robo advisors — real people, who understand your hopes, fears, dreams — who have your back.

I think of StashWealth like a seasoned sherpa, guiding you up Kilimanjaro or Everest. They’re there to tell you when to pause and rest, and when it’s time to push ahead, no matter how tired you are. They’ll be fair weather times, and you’ll wonder, do I really need this guide? I could do this myself!

But then the trail disappears. The wind howls in your ears, and you can’t see your hands in front of you. That’s when you can follow their lead, sticking tight to the trail they blazed for you, even if the path is rail thin and you’re surrounded by icy cliffs on all sides. You can’t see where you’re going, but you don’t have to.

All you have to focus on is putting one front in front of the other, until you’ve weathered the storm, and reached the top of your mountain.

If you’re interested in learning more about StashWealth, click here (non-affiliate link, I get nothing for this StashWealth review, and didn’t tell them I was writing this — just a customer and a fan).

###

Photo Credit: Karen Ro

2 Comments

Fantastic review, Chris. Happy to hear Stash is working out for you!

Thanks man! It is 🙂